Navigating the world of investments can feel like walking a tightrope, especially in today’s unpredictable market climate. The stock market is always uncertain, interest rates are rising and negatively impact bond prices, cryptocurrencies promise quick riches but come with high risks, banks are giving low profits that won’t keep you ahead of inflation and taxes, and real estate is crowded with agents. So, where should I start investing?

One question people often ask me is where to invest or from where should i start investing. This investment advice is sought by people from different backgrounds. Some students tell me they have small sums of money and can’t afford investments that require large amounts, but they are looking for low-risk investments with consistent returns. Others are looking for investments they can afford in installments. Some people with savings want to take risks, while many without pensions or social security want to invest for their retirement. Despite their diverse circumstances, they all have one hidden question: what are the most appropriate investment vehicles for them?

Investment vehicles refer to financial accounts or products used to generate returns. These can include stocks, bonds, real estate, cryptocurrencies, mutual funds, and more. The challenge is choosing the right one to meet individual investment goals. With numerous options available and often limited financial literacy, many people feel confused about where to start. Should they gamble on crypto for quick wealth or engage in stock trading for potential fortune?

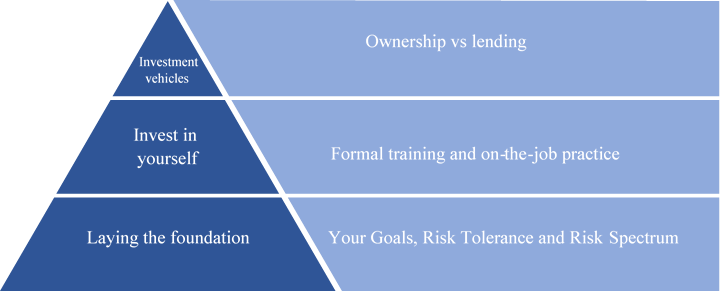

The Investment Pyramid

Based on my experience with investments, I believe that investment decisions should be made in phases, which I call the “Investment Pyramid Approach.” This method treats investing as a long-term endeavour and emphasizes thorough planning. Instead of jumping directly into picking investments like stocks, bonds, or real estate, this approach starts with understanding yourself, your investment behaviour, and your risk tolerance.

The first phase involves a deep self-assessment to gauge your risk tolerance and investment preferences. Are you comfortable with high-risk, high-reward options, or do you prefer more stable, conservative investments? Understanding your risk tolerance is crucial because it shapes your entire investment strategy.

The next phase focuses on enhancing your financial literacy. Educate yourself about various financial products and investment options. This knowledge is essential for making informed decisions and avoiding common pitfalls. Studies have shown that investors with higher financial literacy tend to achieve better returns and make more strategic investment choices.

After building a solid foundation of self-awareness and financial knowledge, you are prepared to embark on your investment journey. This final phase involves selecting the appropriate investment vehicles. Whether you choose stocks, bonds, real estate, or other assets, your prior preparation ensures that your decisions align with your long-term goals and risk tolerance

Phase 1: Laying the Foundation for Successful Investing

In the first phase of investing or to start investing wisely, you’ll need to focus on three key areas: determining your investment objectives, assessing your risk tolerance, and selecting investment on risk spectrum of investments scale.

Understanding Your Goals

The most crucial part of investing is understanding your goals. Why do you want to invest in the first place? The clearer your investment purpose, the better your decisions will be. Many people confuse their investment purpose with the path they take to achieve it. Your investment purpose is your end goal, while the path is how you get there. For example, when I ask people why they want to invest in stocks, they often say, “to make money.” However, this goal lacks a specific end purpose. A more effective approach would be to say, “I want to invest in stocks because I am planning to buy a new car,” or “I want to save for a vacation.”

Without a clear, written purpose statement for your investment, the chances of achieving your goals are slim. As the saying goes, “You cannot hit a target you can’t see.” I’ve seen people in the stock market make a lot of money and then lose it all simply because they didn’t set clear goals for how much they needed to earn in one month, six months, or a year. They made money, but without a profit limit, they kept trading until they ended up in a loss.

Assess Your Risk Tolerance

Many new investors overlook the importance of understanding their risk tolerance when choosing investments. Not every investment is suitable for everyone. Some people are willing to take risks and invest aggressively. This behaviour might stem from their personality, knowledge, or past experiences. These investors can handle quick losses and gains and are open to exploring new investment opportunities, such as cryptocurrency, stocks, or business ventures.

On the other hand, moderate risk investors take a more balanced approach. They have a threshold level of risk in mind and often invest in stocks with strategies to limit potential losses. Their modest approach might result in lower profits, but it helps them avoid significant losses. Typically, they invest in a balanced portfolio that includes a mix of risky and low-risk assets.

Finally, conservative investors are risk-averse. Their main priority is preserving their original investments. Therefore, they prefer risk-free assets like bonds and mutual funds.

Understanding your investment type is a crucial initial step in investing. Remember, investing is not a short-term endeavour. For some, the investment horizon may stretch to 10 to 15 years, making it an integral part of their lives. Choosing an investment that doesn’t match your risk tolerance can lead to frustration. For instance, some people make good money in crypto, but if they aren’t naturally aggressive investors and are doing it based on someone else’s advice, they may experience continuous stress that affects their health.

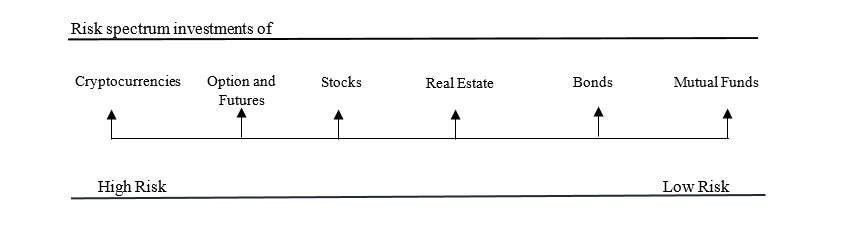

Risk spectrum of investments

If you’ve been following the steps so far, you should have set your investment goals and assessed your risk tolerance. In simple terms, you now understand who you are as an investor and why you are investing. The third and final step in this phase is choosing your assets based on the risk spectrum of investments see figure below.

If your risk tolerance allows for higher risk, you might consider investments like cryptocurrencies, options and futures, and speculative stocks. These high-risk investments can offer significant returns, but they also come with a greater potential for loss. For example, cryptocurrencies have shown immense growth potential, but their prices can be highly volatile .

On the other hand, if you have a conservative risk tolerance, opting for mutual funds or bonds might be more suitable for you. These investments tend to be more stable and provide steady returns over time. Bonds, particularly government bonds, are considered some of the safest investments available .

If you have a balanced approach to risk, you might choose to invest in blue-chip stocks along with some money market securities. Blue-chip stocks are shares of well-established companies with a history of reliable performance, while money market securities offer low-risk, short-term investment opportunities . This combination can provide a balanced portfolio that mitigates risk while still offering growth potential.

Choosing your investments along a risk spectrum is of prime importance. Remember, you don’t start investing with the expectation of significant returns in just one or two months. Investment is a long-term game that requires a long-term approach. I have friends who earn their living solely through stock investing, and they have been doing so for 15 years, continuously investing, learning, and developing strategies. Similarly, one of my acquaintances is a professional currency trader who has been trading for the past six years, and it has become his primary source of income.

The key takeaway here is that the earlier you understand your risk tolerance and identify your preferred investment type, the better positioned you will be in the long term. This understanding is crucial because you may be involved with this type of investment for the rest of your life. Choose wisely, stay committed, and you will be better poised for substantial returns over time.

Phase 2: Invest In Yourself

Most people end up facing losses in their investments because they don’t invest in themselves first. A lack of financial literacy leaves many vulnerable to sales pitches from advisors pushing specific products or services. A 2022 study by the National Financial Educators Council found that poor financial literacy cost Americans an average of $1,389 per person in 2021, highlighting the importance of informed decision-making.

I’ve seen people purchasing insurance products without understanding the simple time value of money, leading them to make long-term payments with the hope of promised returns after 15 to 20 years. A basic understanding of the time value of money could have saved them from such pitfalls. Similarly, I’ve encountered individuals diving into crypto trading solely because a distant friend made a fortune in crypto, hoping to replicate the success. These poor investment choices stem from not investing in one’s skills and knowledge.

There are two main ways to start investing in yourself and prepare for the world of investing: Formal training and on-the-job practice. I remember when I started my first tax consultancy, I invested only PKR 20,000 (around $10) to attend a nine-week practical training on taxes. This was the best investment I ever made, as it led to earning thousands of rupees through tax consultancy over the next few years.

A friend of mine purchased an online training course on forex trading and was ecstatic when she made her first $100. In this digital era, thousands of free and paid courses and training sessions are available on topics like stocks, forex, and crypto. Invest in quality training and learn the art of investing rather than blindly following others’ advice.

If formal training isn’t your style, consider on-the-job practice. One of my students excelled in stock trading by opening an account with a brokerage house, downloading their investing application, and spending time in the brokerage house after classes. He observed how people invested, traded stocks, picked stocks, and decided when to sell, all while studying their psychology. The last time I met him, he was very happy with his progress and the money he was making as a side hustle. So, find your place in a brokerage house, a real estate office, or a crypto trading community.

Phase 3: Choosing The Right Investment Vehicle

The final step in building your investment portfolio is selecting the right investment vehicle. These can be broadly classified into two main categories: Ownership investments and Lending investments.

Ownership Investments

Ownership investments involve buying an asset to become its owner. Examples include real estate, company stocks, and small businesses. These investments often provide both income and capital appreciation. For instance, owning rental property not only generates rental income but also appreciates in value over time. Similarly, start investing in the stocks of growing companies offers dividends and the potential for significant increases in stock prices as the companies expand.

Research indicates that small business investments have created more billionaires in the U.S. than any other type of investment. If you have a high-risk tolerance and are willing to put in the effort, starting your own business can be incredibly rewarding. I have seen students in their 20s launch small businesses alongside their studies and out-earn their professors. The digital age has made starting a business easier than ever, with opportunities in digital marketing, online stores, copywriting, and document editing, among others. A student I know started a document editing business and now manages a team of ten people.

Lending Investments

In lending investments, you lend your money to an entity such as a bank, insurance company, or government. The primary compensation for lending investments is interest. Examples include high-yield savings accounts, Treasury bills, and corporate bonds. While lending investments provide consistent returns, they often only cover inflation and do not offer capital appreciation. This means that over time, the purchasing power of your principal investment may decrease if you consume the interest earned.

Lending investments are suitable for those seeking stable, low-risk returns. They require minimal technical skills and involve lending money to reputable entities with a history of paying promised returns. Examples include national savings certificates, Real Estate Investment Trusts (REITs), and bonds.

Start investing here if you:

✓ Need stability.

✓ Are near retirement.

✓ Prioritize capital preservation.

Prioritizing Your Investments

The key takeaway from this phase is to prioritize your investment options based on your risk tolerance and financial goals. If you are young with an aggressive to moderate risk tolerance, consider starting your own business, even if it is small. The potential for high returns and personal satisfaction is significant.

If you prefer less risk but still want growth potential, prioritize ownership investments such as stocks and real estate. Within stocks, you can choose growth stocks, dividend-paying stocks, or blue-chip stocks. In real estate, you have options like commercial or residential properties, each with its own set of opportunities.

Lending investments should be your last priority unless you seek consistent returns with minimal risk. They provide reliable income but limited growth potential, making them suitable for more conservative investors.

Key Takeaways: How to Start Investing Right

- Test your risk tolerance (Aggressive/Moderate/Conservative)

- Learn first (Courses > Crypto hype)

- Match investments to goals (Ownership vs. Lending)

Remember: Everyone starts investing somewhere – what matters is starting right.